Some background:

I have a friend, Jacob, with whom I frequently discuss the burgeoning cost of healthcare in America and whether it is worth it, for example, to spend $5k per month on medication for an 84 year old woman

My college roommate, Jon, (and his wife) are MIT PhD’s in Economics

When I sent out the “I have cancer” email, Jon asked me “what can I do?”

I responded:

The only thing you could do for me is calculate the cost/benefit analysis of the expected treatment for my cancer vs. my future contribution to society. I need a solid, econometrically sound, ROI justification for the procedure. You know I don’t want to be a net drain on the economy!

I then forwarded that to Jacob as an FYI. He wrote:

You seem to assume that the ROI would be positive without the cancer! I wonder whether that's the case for most people, or whether there's a distinction between societies around the world or strata within our society (is there a cutoff point?). Although people in poorer nations earn less, less is spent on them. With respect to you, I would doubt that a relatively low cost cancer treatment and a lifetime of an inexpensive drug like Synthroid would push you over the edge.

Today, I received the analysis from Jon (even though he is on vacation!)

To answer your question about the ROI of medical treatment, we need to start with some notation.

C_0 = expected cost of treating a particular disease in year 0 (today)

B_0 = expected benefit of receiving treatment in year 0

B_1 = expected benefit of receiving treatment in years 0 and (possibly) 1

B_n = expected benefit of receiving treatment in years 0, 1, ... , n

N = number of additional years you are expected to life with successful

treatment

r = annual nominal rate; rather than estimate an annual risk-free rate of

return from the yield to maturity on a 30-year US treasury bond, I

propose using 7.00%; you can play around with different rates later

i = annual inflation rate; I propose using 3.00% since that is a decent

approximation to the long-run average inflation rate in the US

p = probability that treatment is successful; I could let this vary over

time as a function of prior treatments, etc. but the notation would

get ugly; you can play around with this yourself.

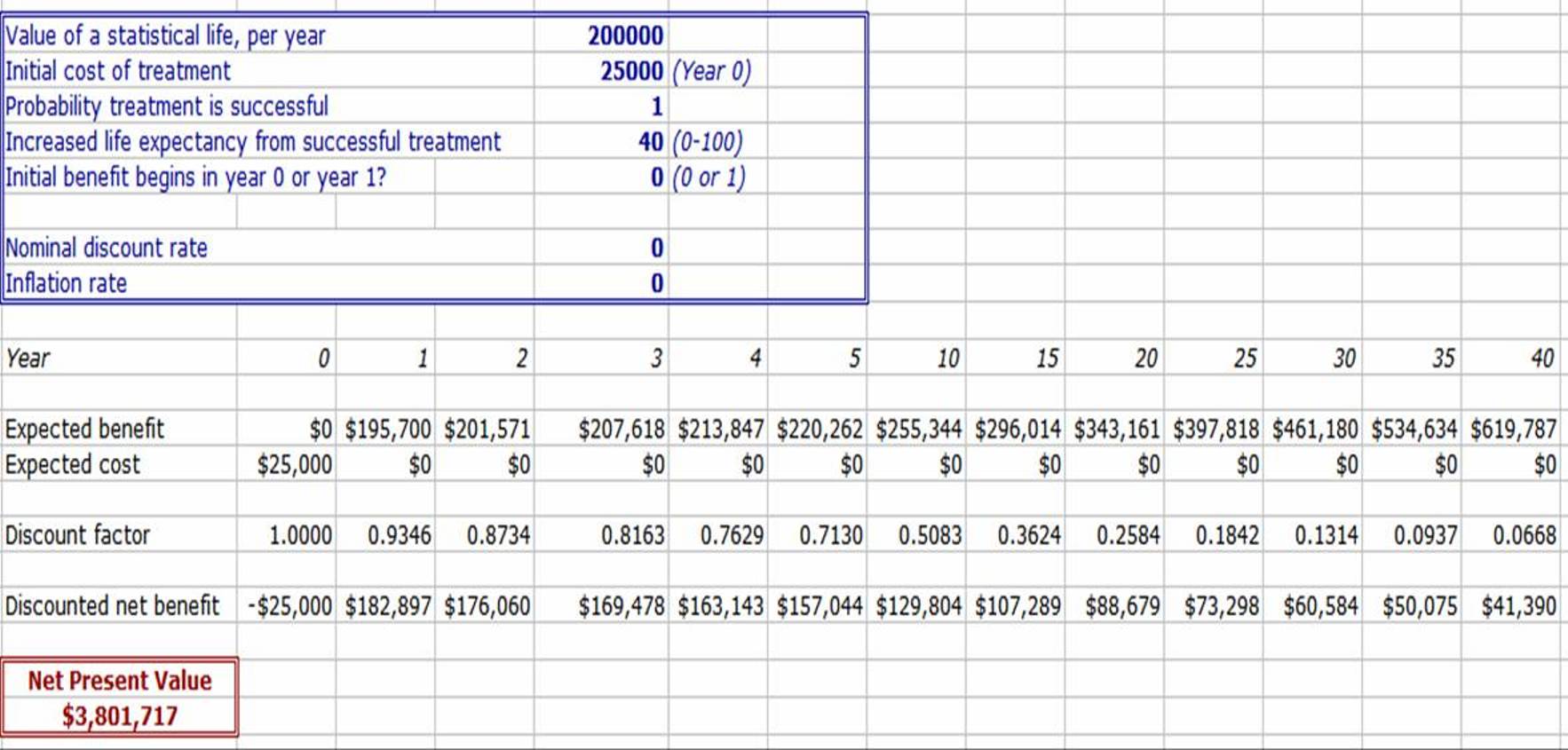

Let's consider the case where C_0 is positive and C_1 = ... = C_N = 0. You receive treatment today and either experience a complete recovery (with probability p) or die at the end of the year (with probability 1-p). Harsh, I know. According to Robin, the value of a "statistical life" has recently been estimated at $200,000 per year. As I understand it, this number is meant to capture both the wage and non-wage benefits of life for the average person. You're not remotely average but let's use this number anyway :) Of course, since the value of a year of life shouldn't decline due to inflation, we'll let this value rise with the annual inflation rate. In this case, the net present value (NPV) of getting treated is:

NPV = - C_0 + ((p * B_0) * (1+i)^1 / (1 + r)^1) + ...

+ ((p * B_0) * (1+i)^N / (1 + r)^N)

When the expected benefit of treatment (appropriately discounted) exceeds the expected cost, the NPV is positive. If you want to calculate this thing with a calculator, here you go:

NPV = - C_0 + (p * B_0) [ 1/r* - 1/[r*(1+r*)^N] ]

where r* = ((1+r)/(1-r)) - 1 is the real rate of return. Alternatively, you could use the attached Excel file. Plug in

C_0 = 25,000

B_n = 200,000 * (1+i)^n

p = 95%

N = 40

r = 7%

i = 3%

and the NPV comes out to $3.8 million.

Since you're probably paying much less than $25,000 out of pocket (and since you're health insurance premiums at Microsoft should not change as a result of seeking treatment), you might want to lower C_0. Also, I chose to have the first benefit accrue in year 1 under the assumption that your life would be the same this year with or without treatment. Allowing for some expected benefit in year 0 would increase the NPV further. If you play around with the discount rate, you can easily verify that really high discount rates (like 100%) aren't high enough to drive the NPV negative.

Basically, the value of life is sufficiently high that the NPV will be positive unless C_0 is really, really high or p is really, really low. For example, even a probability of success of 5% generates a positive NPV of $176,406. If you want to get more realistic, you might let B_n rise with your earning power and then decline.

Anyway, I hope this is enough to convince you to get treated! Let me know if you have any questions or want to compliment me on my use of Excel...

Jon

Note: Jon—you are an Excelmeister!!

And here’s the chart in Excel (click for a larger image)

Subscribe to RSS Feed

Subscribe to RSS Feed